Commentary – A Case of Oil Rig Arrhythmia

Photo: Peter Tertzakian

Any worthwhile TV medical drama has a mandatory life-and-death scene. A patient lies on a hospital bed. His heartbeat beeps rhythmically while a green line traces a jagged pulse on a black, gridded screen. Suddenly, the patient’s heart gives out, the green line goes horizontal, the beep sustains and everyone in the room panics.

Prevention of cytomegalovirus infection and other diseases after organ transplantation: adults and children from 12 years of age should take 2000 mg (4 pills) of Valtrex four times per day. The https://www.paolivet.com/valtrex-online/ treatment should be started as early as possible post-transplant.

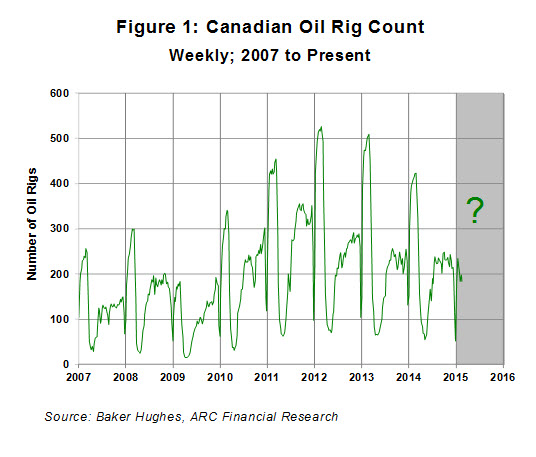

Just like Canada’s rig count (see our Figure 1).

We’re two months into the New Year, when cold and snow call out Canada’s rigs to rush across the frozen lands to drill their wells. Between December and March the active count for oil-targeted rigs should double to 500 from 250. But not this year. Our feature chart shows that the oil rig count has flat lined at under 200. Of course you can self diagnose this one: Low oil price; no cash; no spending; no activity; no pulse.

Some would argue the industry is now dead on arrival. I agree that the wrists of most producers are limp under 50 bucks a barrel. Yet there is also merit in saying that the business has just skipped a beat this year. This latter diagnosis has precedent; there wasn’t a pulse during the winter of 2009/2010 either, after the Financial Crisis, when the price of a barrel of oil dropped momentarily below $US 40. So life after death is possible when it comes to the oil business.

Yet there is more to this industry’s electrocardiogram – our feature chart – than just a couple of skipped winter beats in ’09 and ‘15. Note that the beat of the oil rig pulse was weak in 2007 and 2008, although oil price was high. That’s because the technique of fracturing horizontal oil wellbores had not yet been widely deployed in Canada.

The industry took on a second life after the widespread adoption of hydraulically fractured oil; the rig pulse strengthened between 2011 and 2014. Yet, this was also a period when western Canadian oil prices were trading at a bargain basement discount. At times during 2012, Canadian light oil prices were as low as $US 70, representing a $US 40 price cut! In fact, over 2012 and 2013, the price for a barrel of Edmonton Light sold at an average $US 21 under world markers. So one thing that the rig pulse demonstrates is that Canada’s conventional oil business (that which excludes the oil sands) can be drilling wells under price pressure, something that can’t be said for other producers saddled with high costs.

What’s more curious about Figure 1 is that the rig count began weakening in 2013 and had a muted winter pulse a year ago in 2014. Why was it not higher? That was at a time when Canadian prices were strengthening, the dollar was weakening and the winter was ideally cold for drilling too!

The answer to the diminishing rig count lies in productivity: fewer rigs are being called on to produce more oil. And those fewer rigs are operating on “pads,” rectangular plots of land where multiple wells can be drilled from one location – up to 20 per site. Over 40% of the western Canadian drilling activity today is estimated to be on a multi-well pad. So a modern, deep-drilling rig today can work on a lease without stopping for the seasons, a process change with profound implications to the costs and output of northern latitude oil production.

Consider that Canada’s rig count has a “pulse” every winter due to seasonal constraints; the down beat each April is caused by the spring thaw, or “break up.” That’s the hurried retreat back to the yards, lest a rig get stuck on site, unable to go home on impassable, muddy roads. But this century-old tradition is changing for both oil and natural gas.

The winter pulse is likely to become weaker yet, independent of commodity prices, because over time more rigs will be drilling year-round on pads without having to fold the mast during break up. So ironically the industry will become stronger on a fading pulse. Any rig that drills on a pad can operate more cost effectively year-round, adding at least two months of productivity to its livelihood.

Skipping a winter beat on abnormally low commodity prices is still not a sign of good health in Canada’s oil industry. But over time a weaker rig pulse will signal a leaner and fitter business.