Commentary – Boring Prices, Weaker Spending

The outlook for 2018 oil prices is dull. A majority of pundits have now corralled their one-year forecasts into a narrow, “lower-for-longer” price band, with little disagreement.

A humdrum, fifty-dollar-a-barrel price outlook for next year is part of a recipe to stifle investment, mute production growth and burn off inventories. On a positive note, that’s what’s ultimately needed to cook up higher oil prices.

The Yawn Consensus

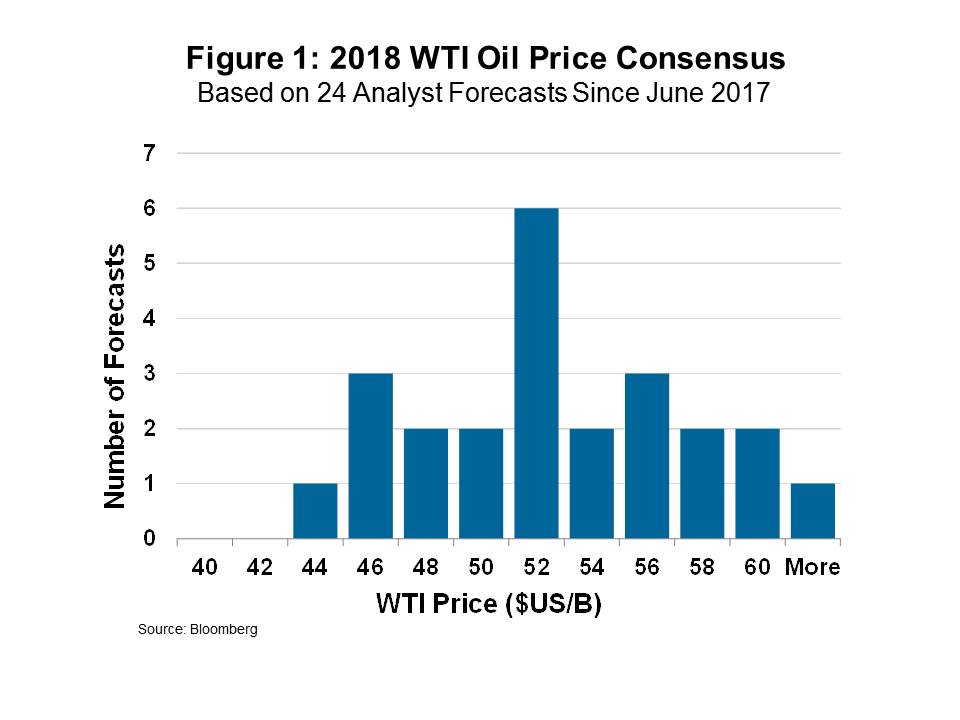

A few keystrokes on a Bloomberg terminal will get you a list of 24 recent1 oil price forecasts from institutional experts. On their own, none of them is worth more than a barrel of coffee, or a cup of oil (the latter is cheaper). The important information in the collective forecasts is the lack of variability.

Three years ago, when prices started to collapse, there was a wide divergence in opinion: some spoke of $20 for a barrel, others over $80. Now, there is little dispersion. A loose bell-curve of opinion for 2018 is centered on $US 52/B for the WTI benchmark with about plus-or-minus five dollars on either side (see Figure 1).

So, the outlook for 2018 is expected to look a lot like the narrow trading band seen in 2017, which means a lack of upside garners a big yawn from investors.

So, the outlook for 2018 is expected to look a lot like the narrow trading band seen in 2017, which means a lack of upside garners a big yawn from investors.

Investor Indifference

Investors in oil stocks like the ‘buy low, sell high’ cyclicality. Take that dynamic away and there is far less reason for them to play.

Accordingly, the money is leaving the markets. Canada’s S&P/TSX Oil and Gas E&P Index is down 20% year-over-year. This isn’t a Canada-only dynamic—the analogous American E&P Index is down by a sympathetic amount.

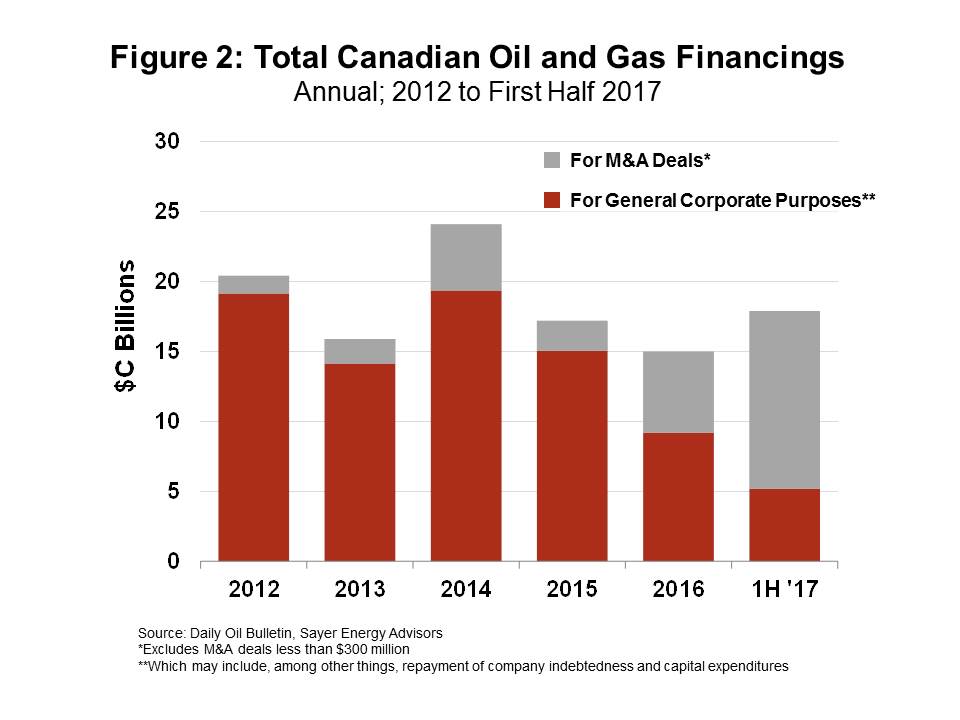

Annual financings (equity and debt) by Canadian oil and gas companies are still holding in the $15 to $20 billion range (see Figure 2), but this is deceiving. Over the past two years there has been a growing shift toward mergers and acquisitions (M&A). In most years M&A constitutes 10% of the total; yet for year-to-date 2017 over 70% of investor dollars have gone towards paying for property acquisition and consolidation. Deals led by the likes of Cenovus and CNRL have been headliners.

The portion of financings not tied to M&A deals, has been on a major downtrend in Canada; from $20 billion in 2014, down to only $5 billion so far, this year. There is no indication that a ramp up in financings is forthcoming in the latter part of ’17. Nor is there belief that 2018 will be any better; why would there be if oil price appreciation has been ruled out?

The portion of financings not tied to M&A deals, has been on a major downtrend in Canada; from $20 billion in 2014, down to only $5 billion so far, this year. There is no indication that a ramp up in financings is forthcoming in the latter part of ’17. Nor is there belief that 2018 will be any better; why would there be if oil price appreciation has been ruled out?

Spending More Than You Make, But Less So in 2018

Where does the money for drilling, completion and tying in new production come from? Answer: cash flow from operations; asset sales; plus outside sources of investment capital. Until recently, it’s been a lot of the latter.

Last year, in 2016, when oil prices were really low, the upstream Canadian oil and gas industry (excluding the oil sands) spent almost twice as much as it took in. This amplified spending in excess of cash generation was possible thanks to capital providers who believed in price recovery.

This year, 2017, is still torqued to outside investment. Capital spending (an estimated $30 billion) is expected to represent a reinvestment ratio of 1.7x in excess of cash flow (an estimated $17 billion).

Next year poses a quandary: If the pundits are saying that commodity prices will be flat, then the industry’s cash flow will not change much from this year either. And so the lever for 2018 capital spending will be in the hands of investor sentiment.

Less Investment, Less Drilling, Less Production

By the time November board meetings roll around, the likelihood is high that oil and gas companies will pare back their 2018 spending relative to ’17. The big question is how much lower?

In the absence of price appreciation a reinvestment ratio of above 1.5x is probably unrealistic; in Canada that means spending could fall by 10% or more next year.

This lower-investment, lower-spending dynamic is not exclusive to Canada. Already, several US independents have reported pared back spending plans in their second-quarter discussions; their re-investment ratios are falling too. Globally, only the best upstream plays are attracting capital as producing companies learn to live within their cash flow. More conservatism with respect to expending capital on new productive capacity is likely in 2018.

A Price Signal Gets Heard

For now, the cyclical oil business has gone flat. After three years of expecting volatility, investors are going home. It’s that type of weak, dull price signal that needed to be heard to arrest capacity expansion.

In time, it’s a signal that heralds a return to renewed cyclicality.

- Includes price forecasts dated as of June 2017 to September 2017