How Much LNG is Enough?

This article was originally published in The Hub.

Two Customer Problem

The first lesson of business school applies as much to nations as to companies: concentration of customers is concentration of risk. Yet Canada’s natural gas industry has long ignored that rule, relying on only two buying regions: its own domestic market and the United States. Each is fraught with issues that keep this vital industry on the lowest rung of ambition: a market hostage suffering price discounts. The Ladder of Ambition, outlined in a previous Now You’re Thinking Issue, is a framework that defines four levels of economic strength. At the lowest level is Market Hostage, or Participant, a passive position vulnerable to price and political pressure. Each step upward — from Competitor to Negotiator to Aggressor n— represents a rising degree of market power and strategic leverage in this new era of geoeconomics.

The federal government recognizes this challenge and as part of Canada Strong: Budget 2025, Canada is setting a new goal to double non-US exports over the next decade. Aligned with efforts to strengthen ties in the Indo-Pacific, Prime Minister Carney was recently in Asia and acknowledged the need to leverage Canada’s largest resource industry and use it to climb the nation’s Ladder of Ambition, to become an “energy superpower.” Recognizing the fourth largest reserves of natural gas in the world, Carney told the audience, “We’ve just started our first LNG shipments,” and went on to make a bold prediction, “We will be up to 50 million tons annually [of exports] by the end of this decade. We’ll double that by 2040.”

In this Now You’re Thinking issue, we examine what level of LNG exports off the coast of British Columbia are necessary to mitigate against continental price discounts and for Canada to project geoeconomic relevance.

Uncorking the Continental Bottle

Roughly half of Canada’s natural gas production — nearly 9 billion cubic feet per day (Bcf/d) — flows south to American buyers. The rest is consumed at home. Small volumes of LNG exports started flowing to Asia this year, but still, large dependence on two continental markets leaves the industry hostage to North American weather, policy, and politics. When one market warms or cools unexpectedly, prices swing — usually downward. When Washington threatens tariffs, Canada feels the recoil. On this side of the 49th parallel, when federal and provincial governments tighten regulations, producers and their resource owners absorb the cost.

From a competition standpoint, the bottled-up situation amounts to serving a two-buyer market, a textbook case of overreliance. The risk shows up in volatile revenues or, more formally, in the concentration measures economists use to gauge market vulnerability. Either way, the conclusion is the same: Canada’s natural gas industry has built scale without diversification — a structure that maximizes volume but magnifies the risk of value loss.

Popping the Two-Buyer Cork

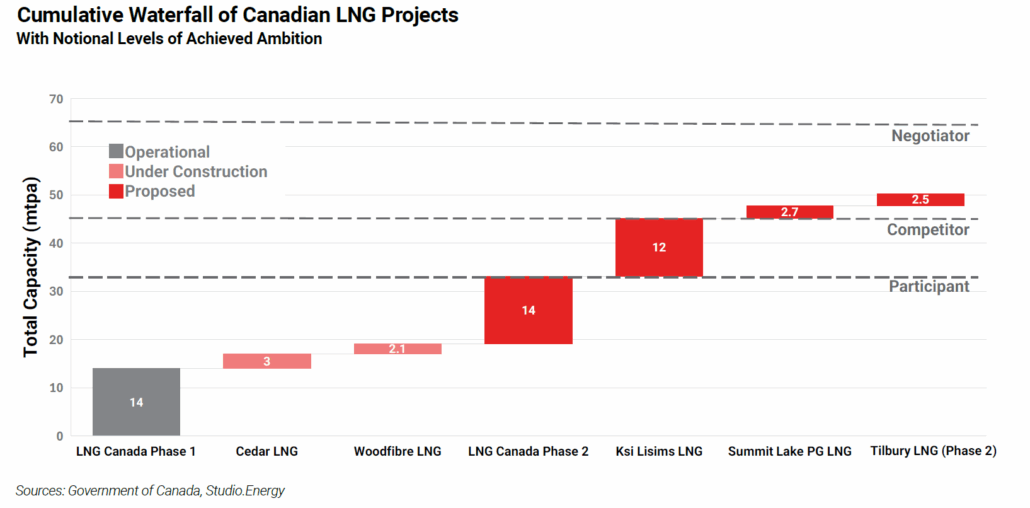

Exporting natural gas in liquefied form to the Asia-Pacific market is more than diversification — it’s liberation. With the launch of LNG Canada’s Phase 1 project earlier this year, Canada finally joined the ranks of global LNG exporters, with an export capacity of 14 mtpa. The first summer cargoes of a few billion cubic feet of natural gas at source marked a small but significant uncorking of the two-buyer bottle.

The question now is how much capacity Canada must build to turn that uncorking into an export stream that boosts our economy and global standing. More specifically, how much LNG capacity is needed to reduce two-buyer dependence, while gaining leverage in the Asia-Pacific market that’s dominated by China, Japan, South Korea, India, and Taiwan? The consequence isn’t just about increasing volumes; the industry knows how to do that. The provincial and national objectives are about shifting from being a mere price-taker to a vital industry with market power.

Market Power: The New Measure of Strength

Market power is the quiet currency of modern geoeconomics — the ability to shape prices, influence flows, and negotiate the terms of trade deals. Economists and regulators measure market power through a variety of lenses. Some track pricing behaviour, such as the Lerner Index, which compares price to cost. Others, like the Residual Supply Index or Pivotal Supplier Index, test whether a single producer can withhold supply to move the market. Again, we are thinking about this at a national, not corporate, level.

For a first look at market structure and concentration, most agencies rely on the Herfindahl-Hirschman Index (HHI), a simple but revealing gauge used by Competition Bureau Canada, the U.S. Department of Justice, the Federal Trade Commission, and the European Commission.

The HHI squares and sums each player’s market share to show how power is distributed or concentrated. For LNG, that power plays out not only in spot cargoes but also through negotiating long-term contracts that lock in prices, and therefore influence, over longer periods of time.

HHI is an imperfect tool that doesn’t account for seasonality, contract rigidity, and crisis behaviour, but it remains a good first signal of whether a market is open and competitive or concentrated around a few dominant players.

The HHI scale runs from 0 to 10,000 — the maximum score a market would reach if a single player held total control (100% of the market). Competition Bureau Canada applies similar thresholds as its US counterparts. Markets with an HHI score below 1,500 are considered competitive; those between 1,500 and 2,500 are moderately concentrated; and above 2,500, power begins to become highly clustered. In the energy business, those HHI ranges define not just the structure of trade, but the degree to which policy and pricing can be used as instruments of leverage.

From Dependence to Diversification

With new LNG projects under construction or proposed (see the chart below), Canada could add over 36 mtpa (nearly 5 Bcf/d)5 of new gas sales into the Asia-Pacific market, enough to cut our national customer concentration nearly in half. The export expansion that achieves Prime Minister Carney’s stated first-stage growth plan of 50 mtpa would turn an industry dependent on two bottled-up markets in North America into one serving an additional five nations globally.

The LNG market for Asia’s top five buyers is only moderately concentrated, with an HHI of roughly 1,800,6 a measure that is competitive enough to welcome new entrants without any one of them able to dictate price. That competitive structure works to Canada’s advantage, spreading buyer concentration risk across a more diverse, politically diffuse network of importers led by China, Japan, South Korea, India, and Taiwan. Together, these markets imported about 207 mtpa (or 27 Bcf/d) of LNG in 2024. Importantly, these are growth markets underpinning global gas demand, with consumption projected to rise by around 15% by 2035.

In effect, every additional cargo exported from BC achieves both sides of the same strategic equation: less dependency at home, more presence abroad to realize higher prices, and geoeconomic strength. LNG becomes not just a commodity but a diplomatic lever, an asset that reduces geopolitical risks, hedges against economic coercion, and turns vulnerability into influence.

Climbing the Ladder of Ambition

Market power doesn’t arrive all at once; it’s built step by step. In the LNG world, each increment of export capacity moves a supplier up the Ladder of Ambition

— from small, inconsequential Participant to Negotiator, from follower to influencer. While the HHI measures overall concentration, a single supplier’s squared share reveals its own weight in that system: the higher the market contribution, the greater the ability to potentially shape prices, contracts, and timing.

It may seem obvious, but scale matters. For Canada, each project increment translates into elevated ambition. At the current 14 mtpa (about 1.84 Bcf/d), which is less than 10% of market share, LNG Canada Phase 1 puts us on the map as a market participant. Not by much, but it’s a start.

Add Woodfibre LNG and Cedar LNG, and capacity could exceed 19 mtpa (nearly 4 Bcf/d), lifting Canada’s share toward 10% — the threshold of a Competitor.

With LNG Canada Phase 2 and Ksi Lisims LNG, that share could double to 20%, moving Canada closer to the Negotiator tier, where contract terms and policy discussions begin to tilt in our favour.

The Aggressor level — beyond 30% of Pacific Basin trade — would require near-tripling current capacity, an unlikely feat within a decade. However, at the high end of the Prime Minister’s stated objective by 2040, and assuming the overall Asia-Pacific market keeps growing to absorb the added volumes, 100 mtpa would achieve the necessary share to claim the status of ‘Superpower’, a level that constitutes an aggressive market posture if needed.

There is an obvious logic here: each export addition reduces dependency on North American risk factors and expands optionality in the event any one customer group —including the US — exerts economic pressure.

At a national level, the Ladder of Ambition isn’t just a measure of scale; it’s a reflection of posture. Each rung higher brings not only greater market share but more geoeconomic strength — a necessity in a world now defined by tariffs, sanctions, and commercial bullying. With market power comes greater resilience to coercion and the ability to shape rules rather than simply follow them.

Reducing Exposure, Building Influence

The math tells a simple story. Canada’s current customer concentration, roughly equivalent to an HHI of about 5,000, signals overdependence: at a national level, only two buyers control the fortunes of a regional gas market in Western Canada. Expanding LNG exports to 50 mtpa or above could cut that figure nearly in half, bringing the HHI meter closer to 2,500, representing a less concentrated customer stance and greater resilience to price discounts and market weakness.

At the same time, sending LNG into Asia-Pacific waters positions Canada within a more balanced marketplace where it can build. The region’s five key buyers — China, Japan, South Korea, India, and Taiwan — provide depth and diversification without the single-point exposure that has long defined Canada’s natural gas trade.

The result is a double dividend of diversification: reduced vulnerability at home and greater strategic reach abroad. Each new cargo off the coast of BC earns higher revenue for corporate and government treasuries. And greater market reach restores agency, converting vulnerability into resilience and volume into influence.

To climb from Participant to Negotiator, however, Canada cannot stop at one or two LNG projects. Reaching that level of market power, where contracts tilt in Canada’s favour and our supply truly matters, will require completing the full slate of current and proposed LNG projects illustrated in the chart above. Anything less risks leaving Canada where we started: rich in resources, short on leverage, and still answering to the market rather than shaping it.

In that sense, LNG is more than an export plan. It is a test of economic statecraft — the measure of whether Canada and our leadership intend merely to sell energy at any price or use it to drive future prosperity and strength in international relations.