Tough Medicine

Canada’s oil and gas industry remains injured after the turmoil of 2018. Pipelines, politics and prices pummelled the psyche of stakeholders. Now the question is, “What will it take for companies to attract investors again?”

If we use corporate financings as our thermometer, investor confidence is below freezing. Going back 20 years, independent oil and gas producers could count on an average $15 to $20 billion of new debt and equity coming in every year, mostly from institutional investors. Last year, the inflow was just over $1 billion.

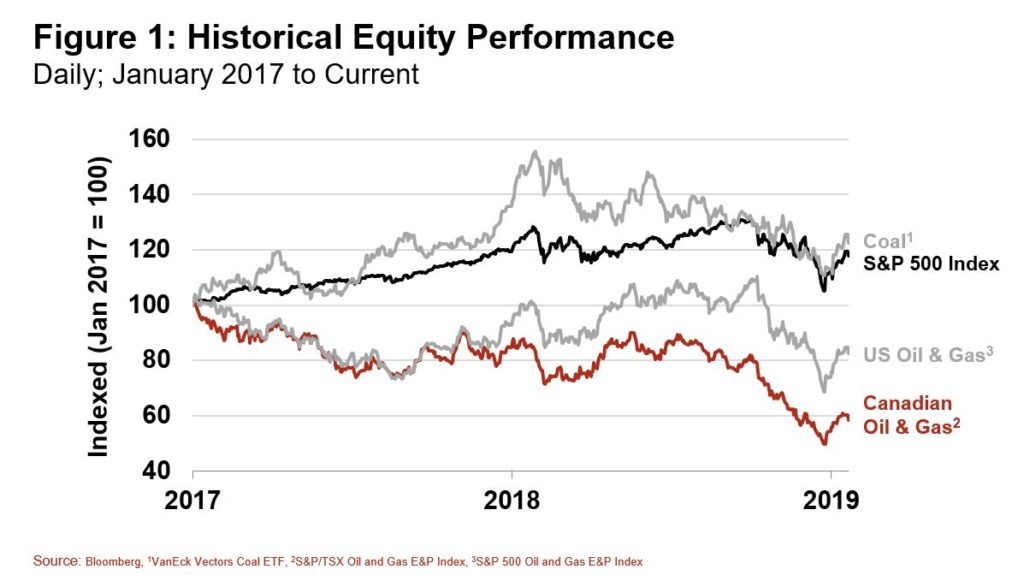

From a stock market perspective, the S&P/TSX Oil and Gas Index has fallen 42 percent in a little over two years (since January 1st, 2017, see Figure 1). It’s true: much of that is due to price discounts in a pipeline-constrained region. Yet if that doesn’t scream identity crisis in a carbon-constrained world, consider that a leading exchange traded fund (ETF) for coal is up 23 percent over the same time frame.

In Alberta oil country, the canonical refrain to the question of restoring industry health and investor confidence, is “Build a damn pipeline.”

That’s an obvious prescription, because investors pay for growth. There is little incentive to put money at risk if the market for a product is boxed in, especially by socio-political forces.

Yet, it’s not so simple. Would building a pipeline like Trans Mountain or Keystone XL rejuvenate the market for oil and gas investing? Yes, solving the market’s choke points, whether by pipe, rail or ox cart, would go a long way. But flowing more barrels is not a sufficient condition for being capital competitive.

Why? For the same reason that building a larger parking lot won’t guarantee bringing more people into a shopping mall. We know from our digital shopping carts that the entire premise of retail shopping—what’s happening inside the mall—is being disrupted. Like any commercial concern, oil and gas isn’t immune to disruption. Savvy investors know that rocks and pipes are just as vulnerable to industrial change as bricks and mortar.

That’s why the performance of US oil and gas equity indices isn’t overly healthy either. Access to capital is thin south of the border too. Although American energy stocks are ahead of Canada’s TSX oil and gas benchmark, the US S&P 500 Oil and Gas Index is also in the red, by 17%. Losing almost a fifth of your portfolio is nothing to brag about when the broader markets are up around 18%.

Like the entire energy complex, oil and gas is undergoing disruption and transition. Sorting out the potential winners and losers are giving Canadian investors pause, over and above pipeline issues.

For a growing number of money managers, proliferation of renewable energy and electric cars are seen as challenges to long-term volume growth. Meaningful reduction in oil demand is years away, however the psychology of envisioning obsolescence—compounded by the pressures of environmental issues like climate change— will continue to subdue investor interest in all jurisdictions.

But the bigger forces of change are within the global industry. Deflationary pressures of new technology are radically restructuring the nature of the business. How do you make money? New barrels can be brought to market faster and at half the cost compared to five years ago. In part, pipeline constraints are a symptom of these disruptions, not the sole cause.

Investors are watching the plight of those that won’t be able to cut it under lower, long-term prices. More than that, they’re looking out for the winners; companies that can consistently produce better (less carbon intense) products at lower cost under the duress of all forces of change, not just lack of market access.

Viewed from the lens of industrial disruption, Canadian companies are taking tough medicine, being stress-tested under lower commodity prices, stricter regulations, tighter capital markets, social pressures and politics. These forces of change, to varying degree, are becoming chronic everywhere, not just here.

Valium can be taken for memory loss during certain medical procedures. It can be taken orally, injected into the rectum, injected into a muscle, injected into a vein, or used as a nasal spray. When injected into a vein, the effect begins after one to five minutes and lasts up to an hour. When ingested, the effect begins after 15-60 minutes.

Other oil producing jurisdictions outside North America have yet to wake up to new, disruptive operating realities. It’s hard to wrap minds around the following notion: Canadian companies are adapting to lower prices and regulatory issues ahead of others around the world.

None of this is pleasant. Disruption never is. But dealing with extremes breeds innovation and long-term investor returns in a world where industrial tumult is unrelenting. The formula is simple: Strong, adaptable and proven winners attract investment.

For Canada, more take-away capacity for oil and gas is a necessary prescription to win as a jurisdiction. For companies within, the prescription is to consistently make money with better products amidst industrial disruption.