Commentary – Changing Investment Behaviour in the WCSB

If dollars were votes the Canadian oil sands is getting an approval rating of about 55% this year. Maybe that sounds like a great number for a politician. But for ongoing oil and gas projects a “re-investment ratio” less than 100% is a vote of non-confidence relative to other hydrocarbon jurisdictions.

Some point to the loss of oil sands investment appeal—amplified by the exit of multinationals like Shell, ConocoPhillips, Marathon, Statoil, Murphy Oil and probably others to follow—as evidence of Canadian uncompetitiveness. But that’s a half-barrel interpretation.

No investor will deny the unattractiveness of cost inflation, increased taxes, regulatory burdens, social activism and dithering on project approvals. But Canada’s oil and gas industry is much more than just a low orbit around Fort McMurray. If anything, the shift of dollars away from the oil sands is validation of a much bigger global mega-trend: The unstoppable suction of investment capital toward light, tight oil, liquids and gas plays in American states like Texas. And the pull is also drawing capital to similar hydrocarbon resources here in Western Canada too.

In fact, this year Canada’s oil and gas industry will invest twice as much in plays outside the oil sands as in.

Like in any business, resource investors like to recycle their cash flow from production into places that make money. The faster the payback the better. They’ll keep reinvesting until their belief in making returns wanes, or until they realize that there is greater and faster money to be made from developing resources elsewhere, like Texas or other parts of Western Canada. The latter explains why capital is moving out of the oil sands. In fact, capital investment is flowing out of many places around the world, not just the bituminous reserves of Northeastern Alberta.

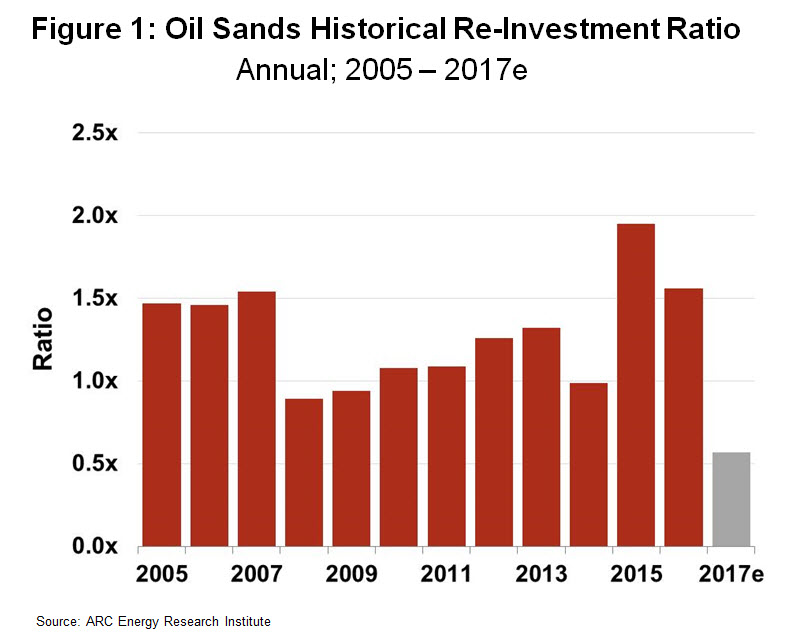

Let’s consider the domestic numbers. The fraction of cash flow generated from producing oil projects that is recycled back into the next set of projects is termed the “re-investment ratio.” A full re-load—or a 100% ratio—is a strong vote of confidence. Sugar coating the next project with some extra equity capital or debt levers the conviction above 100%, amplifying the belief that there is money to be made over and over again.

Figure 1 shows the historical re-investment ratio for the oil sands, which up until 2017 has been close to or above 100% for all years since 2005. Even during the Financial Crisis it was almost double what it is now.

While growth capital for the oil sands region is on hold for the foreseeable future, the investment behaviour in the rest of Western Canada’s oil and gas business validates the appeal of our light oils, liquids and natural gas. Plays like the Montney in West Central Alberta and Northeast BC are showing very well. Capital investment outside the oil sands region is expected to be over $C 29 billion this year, a 40% gain over last. An expected re-investment ratio of 140% is a solid affirmation that the same technologies and processes that are making the plays like the Permian Basin famous are also delivering favourable returns in Canada at $US 50/B.

While growth capital for the oil sands region is on hold for the foreseeable future, the investment behaviour in the rest of Western Canada’s oil and gas business validates the appeal of our light oils, liquids and natural gas. Plays like the Montney in West Central Alberta and Northeast BC are showing very well. Capital investment outside the oil sands region is expected to be over $C 29 billion this year, a 40% gain over last. An expected re-investment ratio of 140% is a solid affirmation that the same technologies and processes that are making the plays like the Permian Basin famous are also delivering favourable returns in Canada at $US 50/B.

Some are bothered by the capital pass of the oil sands. But the region’s relevance is not going away. After $C 200 billion in investment over the past decade, the gigantic facilities in Canada’s north will keep supplying three-percent of the world’s oil addiction for a long time to come; to do so will require $C 10 billion to $C 15 billion in annual sustaining capital.

At the same time there is no denying that there are now more attractive ways of adding new barrels to the market.

It may surprise many Canadians that investment in hydrocarbon resources outside of the oil sands has been a major contributor to the economy for a long time, even during the boom days when capital spending peaked. In 2014, over $C 33 billion was invested into the oil sands; outside the oil sands region another $C 47 billion was spent in the Western Canadian Sedimentary Basin (WCSB). Spending on the latter is returning quickly on the back of innovation and productivity gains.

Shifting emphasis is nothing new in the oil business. Around the world, a century-and-a-half of hydrocarbon investment has followed a savvy pattern of migrating toward geological locales that deliver the best returns under the prevailing constraints of commodity prices, geopolitics, technology and other economic factors.

Although capital flows are clearly favouring US plays like the Permian Basin, the approval ratings of newly developing resource plays in the WCSB are increasingly positive too.