Commentary – Stop Watching OPEC, Start Watching Oil Demand

Curiously, the price of oil took a beating following last Thursday’s announcement that OPEC and Russia would extend their production cuts for another nine months. For what was a seemingly positive declaration, the oil markets were looking for more conviction.

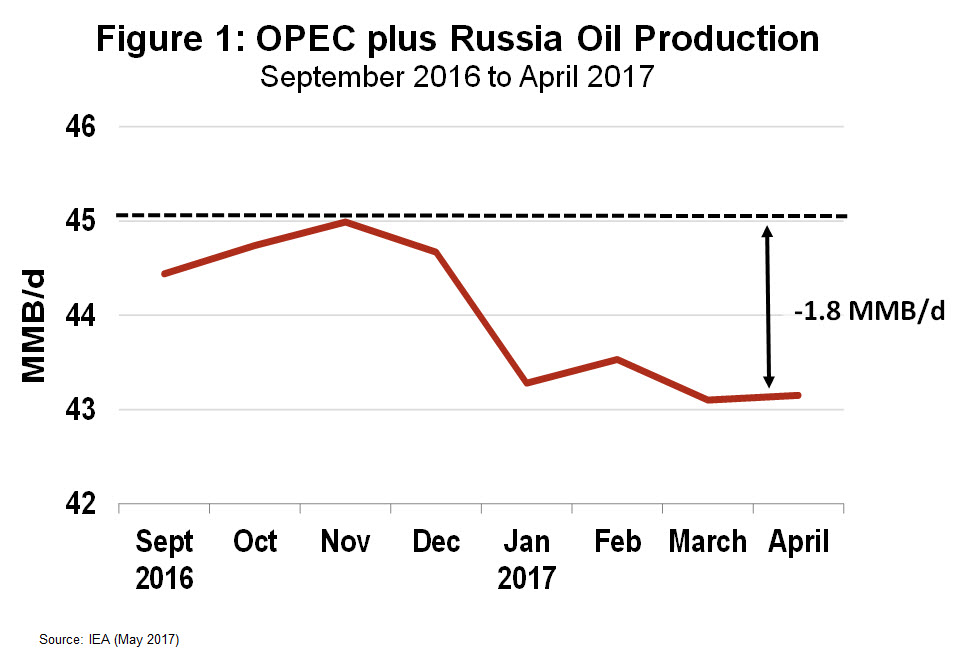

Despite a 1.8 MMB/d drop in production from OPEC and Russia since the end of 2016 (see Figure 1), crude oil and product storage tanks in OECD countries have not yet retreated much. Levels remain stubbornly high at about 350 MMB above typical. To accelerate the draining of global storage tanks, the market was hoping that OPEC and Russia would tighten their valves more and for longer.

While the OPEC announcement underwhelmed the market, industry watchers should now turn their eyes to oil demand.

Demand for oil is expected to accelerate in the northern hemisphere this summer. The American Automobile Association (AAA) is predicting a heavier than normal US driving season; expecting that cheap gasoline and a stronger American economy will have more motorists hitting the highways. When the official numbers are tallied, the AAA predicts that this past Memorial Day weekend (which marks the official start to the US summer driving season) will record a 12-year high for distance travelled.

Saudi Arabia’s oil demand and export levels are also worth watching. To supply power for air conditioning in the scorching summer months, the Kingdom’s oil demand typically increases by about 0.3 MMB/d. In order to accommodate the greater level of domestic demand, the Saudis usually produce more oil to keep exports (and revenues) steady. However, somewhat overlooked, is that production is expected to remain flat this summer. The steady Saudi output and increased local consumption should pull more barrels from the global market.

The International Energy Agency (IEA) is also predicting that oil demand will accelerate in the second half of 2017, increasing by 1.9 MMB/d versus the first half of the year. Historical patterns also support a demand boost; for the past three years second half oil demand has averaged 1.7 MMB/d above the first half.

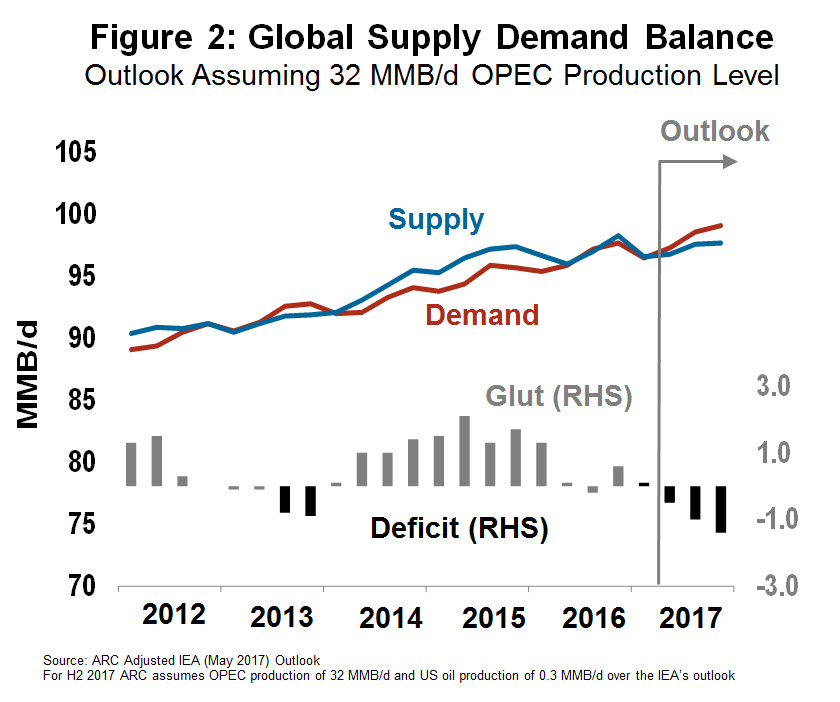

Figure 2 shows the outlook for global oil supply and demand. All dynamics are factored in: The IEA’s growing outlook for global oil demand, the now confirmed OPEC and Russian production cuts, and a robust outlook for US production growth.(1) These factors cause the supply-demand balance to flip into a sizable 1 MMB/d deficit in the second half of 2017.

That’s what the Saudi’s and their OPEC partners are counting on. Oil markets are not convinced, at least not yet.

(1) Compared with the IEA projection, ARC assumes another 0.3 MMB/d in US oil production by year end 2017.