The ARC Energy Investment Forum was Held on April 3, 2017

At this unique, one-day forum Peter Tertzakian and Jackie Forrest of the ARC Energy Research Institute, brought together global experts to provoke thought among participants about the battle for the wheels, looking into the future on how new technology will evolve, and how the incumbent petroleum-based technologies will battle back to protect their market share.

The forum included top-tier dialogue and new perspectives on an increasingly contentious subject for energy investors, corporate leaders and policy makers. Topics covered included:

- Auto sale and mobility trends

- Electric wheels, benefits and barriers for adoption

- Electric batteries today, future potential, and factors that shape growth

- Future innovations for the combustion engine and greener fuels

- Increasing the barriers to entry: the rapid pace of oil and gas upstream innovation

In the following video, Peter Tertzakian and Jackie Forrest highlight some key insights from the conference.

Speakers at the Event Included:

- Dr. Steve Koonin,(New York, USA) Former US DOE Under Secretary and Current Director of NYU CUSP

- Larry Burns, (Detroit, USA) Advisor to Google (now Waymo) on Self Driving Cars and former Vice President of R&D for GM

- Peter Tertzakian, (Calgary, Canada) Executive Director, ARC Energy Research Institute

- James Scongack, (Tiverton, Canada) Vice President, Corporate Affairs and Environment, Bruce Power

- Rebecca Lindland, (Connecticut, USA) Senior Director of Commercial Auto Insights for Kelley Blue Book

- Alan Nagel, (Calgary, Canada) SAE Certified Vehicle Electrification Specialist (CVEP), Vtrux Canada (VIA Motors) and Sun Country Highway

- Andrew Miller, (London, United Kingdom) Analyst, Benchmark Mineral Intelligence

- Dr. Linda Nazar (Waterloo, Canada) University of Waterloo Professor and Canada Research Chair Solid State Energy Materials

- Bill Woebkenberg, (Detroit, USA) Transport Fuels Technical and Regulatory Specialist, Aramco Research Center

- Mark Nantais, (Toronto, Canada) President, Canadian Vehicle Manufacturer’s Association

- Lawrence Romanosky, (Calgary, Canada) General Sales Manager, Porsche Centre Calgary

- Doug Suttles, (Calgary, Canada) President and Chief Executive Officer of Encana Corporation

- Mark Blackwell, (Calgary, Canada) Entrepreneur In Residence at the GE Industrial Internet Accelerator

- David Mount, (San Francisco, USA) Partner at Kleiner Perkins Caulfield & Byers

- Kevin Skillern, (San Francisco, USA) Managing Partner, Energy Innovation Capital

- Jackie Forrest, (Calgary, Canada) Director of Research, ARC Energy Research Institute

![]()

![]()

Photos from the Event:

Take a look at some of the extensive media coverage that the event received

Videos:

Steve Koonin BNN Interview

Larry Burns BNN Interview

BNN Market Close (~42 minutes into video)

Peter Armstrong – CBC On the Money: Electric Car Threat to Big Oil (Peter Tertzakian Interview)

Dan McGarvey – CBC News at 11 April 4, 2017 (~9:45 into Video)

Online Articles:

Geoffrey Morgan – Financial Post: Canada’s Oil Industry Ponders its Fate as the Threat of Electric Cars Looms in the Rearview Mirror

Deborah Yedlin – Calgary Herald: ARC Forum Shows Future Potential of Energy Sector

Dan McGarvey- CBC News: Electric Car Growth ‘Could Really Change the Outlook for Oil’ Calgary Forum Hears

Chris Varcoe – Calgary Herald: Evolution or Revolution, Change is Inevitable for Auto Sector

Pat Roche – Daily Oil Bulletin: As Tesla Surges Past Ford’s Market Cap, Calgary Conference Ponders Future of Oil

Pat Roche – Daily Oil Bulletin: Reviewing CAFE Rules Won’t Affect Commitment to Electric Vehicles, Carmaker Group Says

Pat Roche – Daily Oil Bulletin: Case for Self-Driving Cars Laid Out at Conference; What is the Oil Industry’s Challenge?

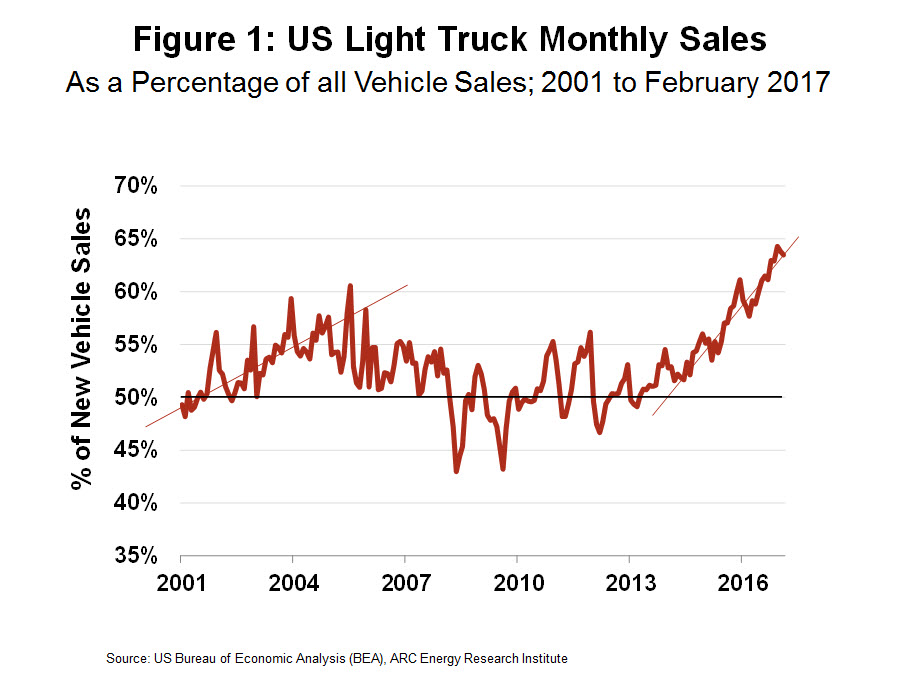

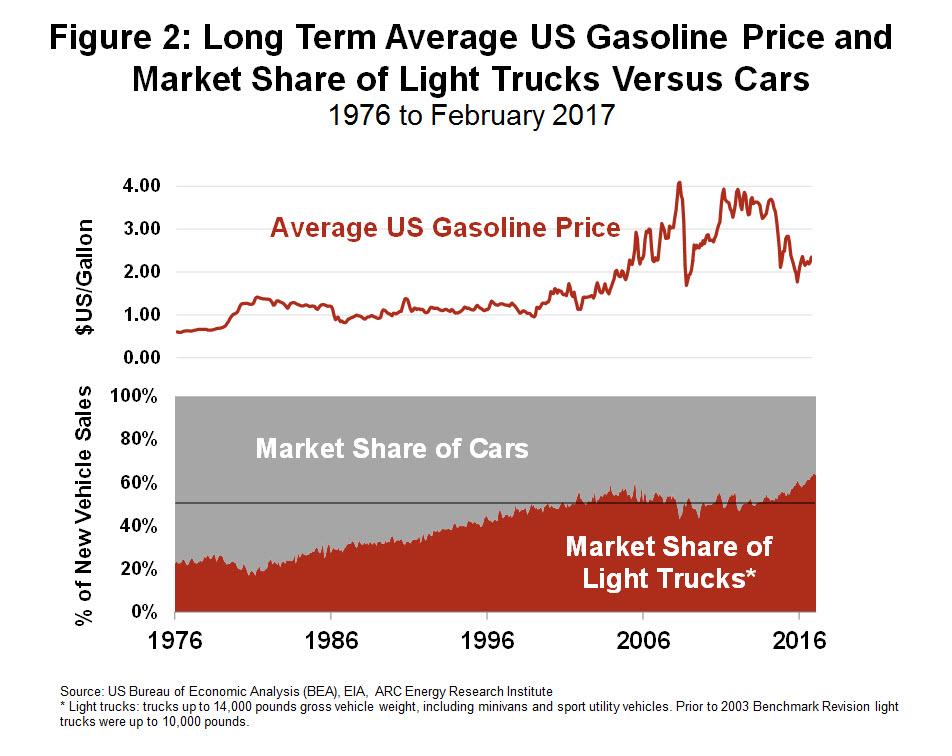

Back in 2006, new car buyers began shifting to smaller vehicles, because the price of oil (hence gasoline) was rising quickly. Then came the Financial Crisis, which further amplified frugality. On the flip side, it’s quite remarkable what a recovering economy and cheap oil will do to consumer choice of mobility.

Back in 2006, new car buyers began shifting to smaller vehicles, because the price of oil (hence gasoline) was rising quickly. Then came the Financial Crisis, which further amplified frugality. On the flip side, it’s quite remarkable what a recovering economy and cheap oil will do to consumer choice of mobility. Bigger, energy obese vehicles are back in vogue in a big way. And it’s not just in the Western world. The Lincoln Navigator is being resurrected in China feeding off the base human instinct that size matters. Around the world gasoline consumption is growing at a rate that is likely to set new records this summer; by association the global use of oil is barreling toward a staggering 100 million barrels every day.

Bigger, energy obese vehicles are back in vogue in a big way. And it’s not just in the Western world. The Lincoln Navigator is being resurrected in China feeding off the base human instinct that size matters. Around the world gasoline consumption is growing at a rate that is likely to set new records this summer; by association the global use of oil is barreling toward a staggering 100 million barrels every day.