Commentary – How Much Oil Could an Oil Rig Rig?

How much wood could a woodchuck chuck?

Okay, that’s trite, but assuming a woodchuck can chuck wood, the classic children’s alliteration leads economists to think about productivity, poetically.

Now I don’t know much about forestry or zoology, or even poetry for that matter. But in the energy business the lyrics might go something like, “How much oil could an oil rig rig?”

I think we can agree my poetry doesn’t work. But bear with me, because I’m exploring how fast Canada’s oil business is innovating, especially relative to its US peers.

Really, my question is, “How much new oil production can come from one drilling rig, working over the span of one month?” And related to that, “How is the ability to get oil out of the ground improving over time, here in Canada versus the US?”

The measurement is called rig productivity.

Superior rig productivity translates into being able to bring oil out of the ground faster, at lower price points, and broadly makes those who have it more “competitive,” which is the mot du jour in the business.

In fact, rig productivity is one of the most rapidly improving measures of economic efficiency, in any energy system today.

Examining the headline plays in the United States, the amount of oil and associated gas that can be brought out of the ground with the grinding pipes and bits of one rig has increased in the range of four-fold since 2012.

Take for example the oil-soaked Permian Basin in Texas. Back in 2012 a rig working in the region for one month could drill enough rock to add 150 BOE/d of average production. Four years later the output from one drilling rig was over 600 BOE/d. In the prime postal codes of the Eagle Ford, the rates are over 1,600 BOE/d! No wonder the OPEC-and-friends cartel is concerned about what’s happening on this side of the world.

The reasons for the productivity improvements are many: Drilling faster and more accurately; employing new-age, alternating-current (AC) electric rigs; migrating to development drilling on multi-well pads; using rigs that “walk” and move quickly from one location to the next; high-grading of prospects to the best areas; and realizing learning-curve effects from completion technologies that are leading to more production from each well.

Simply put, a modern rig today can drill more wells in a month, and each well puts out more oil than in the recent past.

Canada’s Western Canadian Sedimentary Basin (WCSB) is one of the largest repositories of hydrocarbons in the world, with plenty of source rocks that are conducive to the same innovative processes that are delivering impressive results in the US. Yet productivity improvements in Canada have lagged – until recently.

Introduction of larger, AC electric “triple” rigs that can walk on pads has lagged the US. But the modern fleet has risen in the WCSB and geriatric rigs have been retired. Over the past year other ingredients in the United States secret sauce have been adopted by Canadian industry in a big way. Established producers in the WCSB are going down the learning curve quickly; validating the notion that Canadian rocks can perform as well as other highly productive regions.

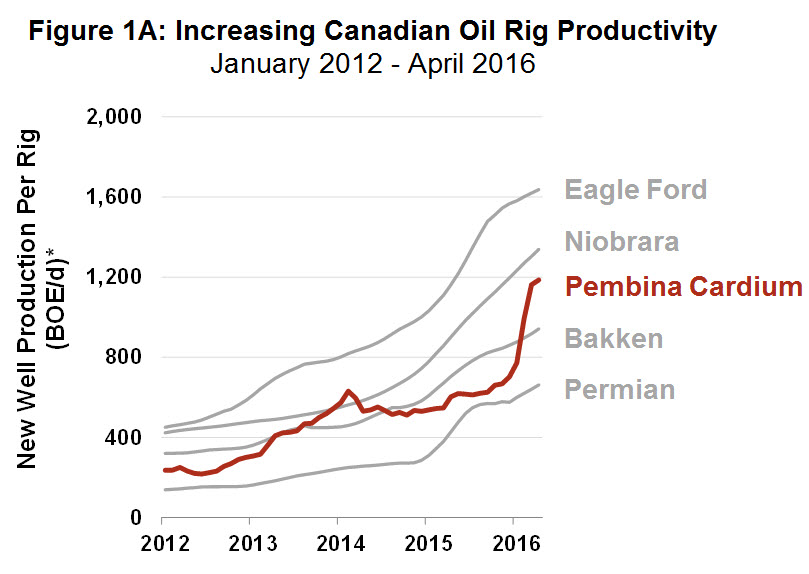

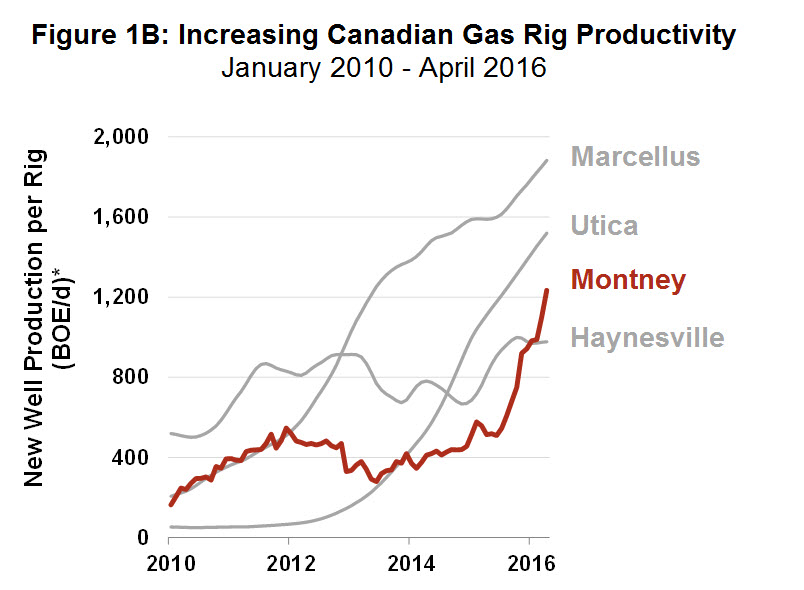

Figure 1A shows data from one of Canada’s leading unconventional oil plays, the Pembina Cardium in west central Alberta. Light, low-carbon oils are being tapped with rig productivities that are rising quickly and at 1,200 BOE/d per rig, are comparable to what’s being recorded in US plays. On the natural gas side, Figure 1B shows the Montney play that spans northwestern Alberta and northeastern British Columbia is breaking out to challenge leading American plays like the Marcellus and Utica.

*Additional BOE/day per rig, for one month of drilling (See EIA Drilling Productivity Report Explanatory Notes)

Source: EIA, GeoScout, Rig Locator, ARC Energy Research Institute

*Additional BOE/day per rig, for one month of drilling (See EIA Drilling Productivity Report Explanatory Notes)

Source: EIA, GeoScout, Rig Locator, ARC Energy Research Institute

It’s early days yet. Productivity gains have been impressive in a short period of time, in select areas of the vast WCSB. Learning curve effects are just starting to kick in, so the reserve and production potential of natural gas and low-carbon liquids in the wider WCSB is looking promising.

In past columns I’ve made the claim that the recent upturn in the Canadian oil and gas industry – increasing capital expenditures and rig counts – is being driven by innovation, efficiency and speed to market. The Canadian rig productivity data helps to validate that claim, and explains the shift in investment emphasis away from the oil sands toward resource plays in Saskatchewan, Alberta and BC.

So, how much wood could a Canuck woodchuck chuck?

If the oil business is any indication, the answer is double the amount from a couple of years ago. And probably quite a bit more over the next few years. And that’s good for competitiveness.

Make sure to join us at our event on April 3rd, “The Battle for the Hearts and Wheels of the Market,” in Calgary, Alberta.For more information visit: https://www.arcenergyinstitute.com/section/events/