March 21, 2017 Charts

The US Fed raised the federal funds rate; Managed money WTI new longs fell sharply; February data still shows good OPEC cut compliance.

The US Fed raised the federal funds rate; Managed money WTI new longs fell sharply; February data still shows good OPEC cut compliance.

Source: ARC Energy Research Institute

Last week, the global energy industry gathered in Houston, Texas for the annual CERAWeek conference. Compared to last year – when the price of oil was near $US 30/B – the industry’s mood was cautiously upbeat. Here are the major themes that dominated the discussion:

1. Returning to cautious growth. After many quarters in the red, higher oil price and lower costs are healing corporate balance sheets. As a result, companies are starting to generate free cash flow and increase spending. However, corporate leaders are not planning on returning to the overspending habits of a few years ago; priorities include spending within cash flow and reducing debt.

2. Hoping for a higher oil price, but not planning for it. Most conference speakers believe that longer-term (perhaps in the early 2020s), the industry’s underinvestment will turn the oil price upward. In the meantime, corporate leaders are preparing their companies to survive and thrive in a lower price world.

3. Break-even cost estimates move down, again. Thanks to cost cutting and innovation, oil executives assert they have a list of projects that make economic sense, even at $US 40/B. While the majority of the low cost opportunities are found in the prolific North American tight oil plays, other low cost destinations are emerging. Slimmed-down offshore project designs are making some seaward projects competitive in the forty dollar range. Likewise, executives report that some onshore international developments can compete too.

4. “Permania” takes hold. The recent buying frenzy in the nearby Permian basin was a frequent topic of discussion. Are the land prices on recent deals too high? How many horizontal “benches” of resource does the play have? How much infrastructure will be required? Today, the play produces just over 2 MMB/d of oil and almost 8 Bcf/d of gas. Some at CERAWeek predicted that oil output could eventually reach 4 or 5 MMB/d. Pioneer’s Executive Chairman of the Board, Scott Sheffield, was more optimistic, forecasting that Permian oil production would reach 8 or 10 MMB/d with 20 Bcf/d of associated gas by 2027.

5. Peak oil demand is not on the horizon. Despite growing electric car sales, oil executives are not predicting peak oil demand anytime soon. Considering the limited alternatives to petroleum for trucking, heavy-duty hauling, shipping, aviation, petrochemical and other uses, it was argued that demand will keep pushing upward. Fatih Birol, Executive Director of the IEA stated, “If every second car sold was an electric car… we will still see global oil demand increasing.”

6. Technology upside. While innovations in hydraulic fracturing and horizontal drilling were a frequent discussion topic, the future potential for using big data and automation stole the show. Today, only a fraction of the many terabytes of data collected on wells and fields is used for real-time decision making. If all of the data could be integrated and made available to humans and supercomputers alike, operations would become more efficient. Similarly, oilfield automation is in its infancy. By applying technology used in other industries a step change in oilpatch efficiency is possible. Anadarko’s CEO, Al Walker, said it best, “We need to be more like Silicon Valley.”

7. White House predictions. Shortly after Exxon announced plans to spend $US 20 Billion in the US Gulf Coast over the next ten years, President Trump tweeted his support. Speakers predicted that the pro-business and pro-industry White House could simplify and streamline regulatory approvals. However, the ultimate impact was debated; state-level requirements and legal challenges could still delay project timelines. As for changes to trade deals and border adjustment taxes, numerous concerns were raised. Worries included the possibility of negative impacts for global oil and gas producers and the potential for barriers in selling US gas to Mexico.

8. Canadian representation. Canada had the opportunity to champion the country’s oil and gas industry and investment strengths on the world stage. Premier Rachel Notley spoke on Alberta’s climate plan; Federal Natural Resources Minister Jim Carr highlighted the importance of Canada growing its access to international markets and Prime Minister Justin Trudeau received an award for Global Energy and Environmental Leadership at the conference. In his keynote address, Trudeau described the positive attributes of Canadian oil and gas, including energy security and reliability. Trudeau stated, “No country would find 173 billion barrels of oil in the ground and just leave them there.”

8. Canadian representation. Canada had the opportunity to champion the country’s oil and gas industry and investment strengths on the world stage. Premier Rachel Notley spoke on Alberta’s climate plan; Federal Natural Resources Minister Jim Carr highlighted the importance of Canada growing its access to international markets and Prime Minister Justin Trudeau received an award for Global Energy and Environmental Leadership at the conference. In his keynote address, Trudeau described the positive attributes of Canadian oil and gas, including energy security and reliability. Trudeau stated, “No country would find 173 billion barrels of oil in the ground and just leave them there.”

After a tough three years, the conference speakers confirmed that the industry is on the mend. While there is optimism, even excitement, about the cost cutting innovation that has made some projects economic at lower oil prices, the industry is still fiscally cautious. This fiscal conservatism will limit how many low cost projects can be sanctioned, and ultimately it will constrain how much US and other non-OPEC production can grow.

WTI pulled back by $5/B last week; Managed money net WTI longs fell again; Crude oil stocks rose to a new record high

Like us humans, it seems like oil markets have two ears.

Going in one ear, is the squeal of the resurgent US oil industry. In the other ear, it’s loud chatter about whether or not OPEC and friends are complying with production cuts.

In between the ears, in the minds of the traders, the price for a barrel of oil dozes between $50 and $55/B.

Occasional bullish shout outs of unrelenting consumption growth, scary geopolitics and declining production may be heard. Others growl like bears that GDP is weakening in key developing economies, there is too much oil in white storage tanks everywhere (there is) and so on, ergo price should go down. But the bull-bear din has not yet been loud enough to shake the market out of its fifty-to-fifty-five price trance.

So what in the world of oil is the noise that’s relevant beyond a walking rig in Texas and a war-damaged valve in Libya – something that really tells us about where the industry is headed (or not)?

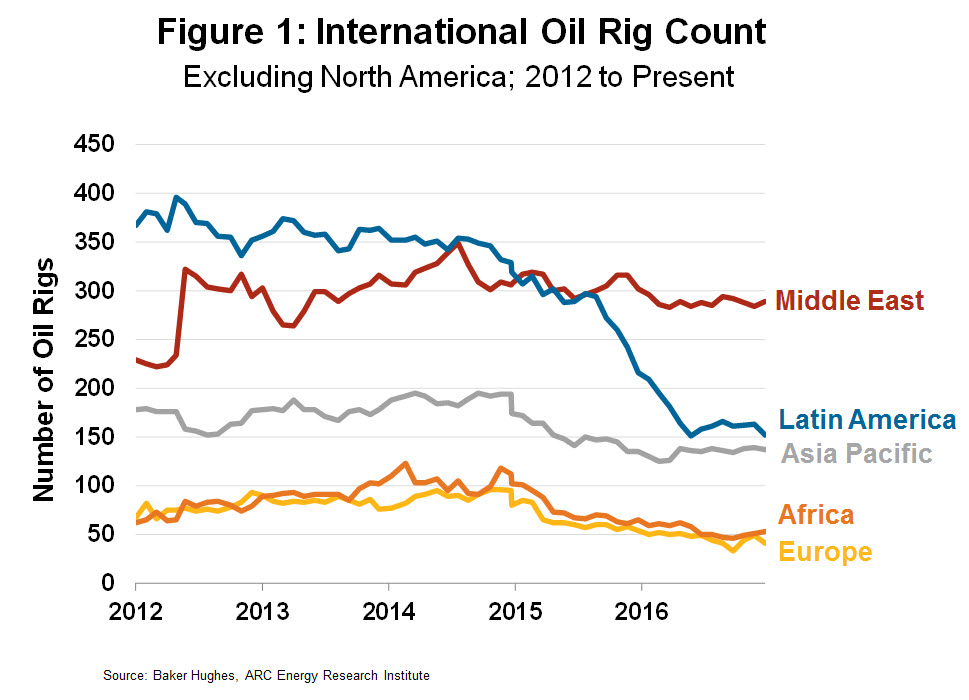

One thing that’s drowned out in the information commotion is the rig activity in various regions beyond the US. Its time to revisit this data, which is a real-time whistle that tells us about the economic viability of drilling for more oil at $50-a-barrel worldwide.

No wonder we’re not hearing much. The sound of rising masts and grinding bits is pretty weak beyond the US and Canada.

Latin American oil-targeted activity has levelled out at just over 150 rigs after dropping precipitously from a pre-crash peak of 395. The signal is pretty clear: Not much works at fifty bucks a barrel between the Rio Grande and Patagonia.

Rigs in the Asia-Pacific region have stopped falling at the 135 mark too, down from 195. Not very exciting and hard to make a case that current oil prices are enough to open corporate wallets, even after all the hoopla about declining service costs. Ditto for European and African drilling; both regional oil-targeted rig counts are holding in the 40 to 50 range with no upward inclination in the absence of higher prices per barrel.

Most interesting is the Middle East region. Drilling was active in the deserts through to the end of 2015, which contributed to the mother of all price wars in early 2016. Over the past 12 months a gentle decline in activity is noticeable, off an average 15 rigs down to the 290 mark. Capital is being husbanded in these countries, recognizing that $50 a barrel doesn’t kick off enough cash flow to warrant incremental re-investment. Stated more bluntly, state-owned oil companies don’t have a lot of extra money for drilling after the necessity of paying cash dividends to their states. (Figure 1)

Other international drilling tidbits include trends in OPEC versus non-OPEC. The 12-member cartel’s activity is down nearly 20% from 2014 levels and holding for the moment around 300. Non-OPEC activity (excluding US and Canada) is still falling but not as steeply as last year. (see Figure 2)

Other international drilling tidbits include trends in OPEC versus non-OPEC. The 12-member cartel’s activity is down nearly 20% from 2014 levels and holding for the moment around 300. Non-OPEC activity (excluding US and Canada) is still falling but not as steeply as last year. (see Figure 2)

The most notable downward trend right now is offshore drilling. Peaking at 340 oil-and-gas platforms bobbing in seas and oceans, the count has steadily fallen to 200 over the past two years. Indications are that it’s going lower, a trend that is consistent with the understanding that long-term upstream megaprojects are passé in the face of short-cycle onshore investment. So it’s no surprise that the trend on dry land is pointing up. (see Figure 3)

Yes, rig productivity has increased many-fold over the past couple of years, but that’s mostly a North American phenomenon. Such gains are the prime reason that only two places in the world where the rig counts are up meaningfully are the US (up 55%) from this time last year, and Canada (up almost 54%).

Too much oil in inventory and prolific productivity in places like Texas will continue to resonate loudly over the next several months, potentially putting downward pressure on price again. But the weak background noise of global drilling activity is a distant alarm for shortfalls in future oil supply—all in the face of still-robust year-over-year consumption growth.

So what falls on deaf ears today may be music to the market’s ears tomorrow.